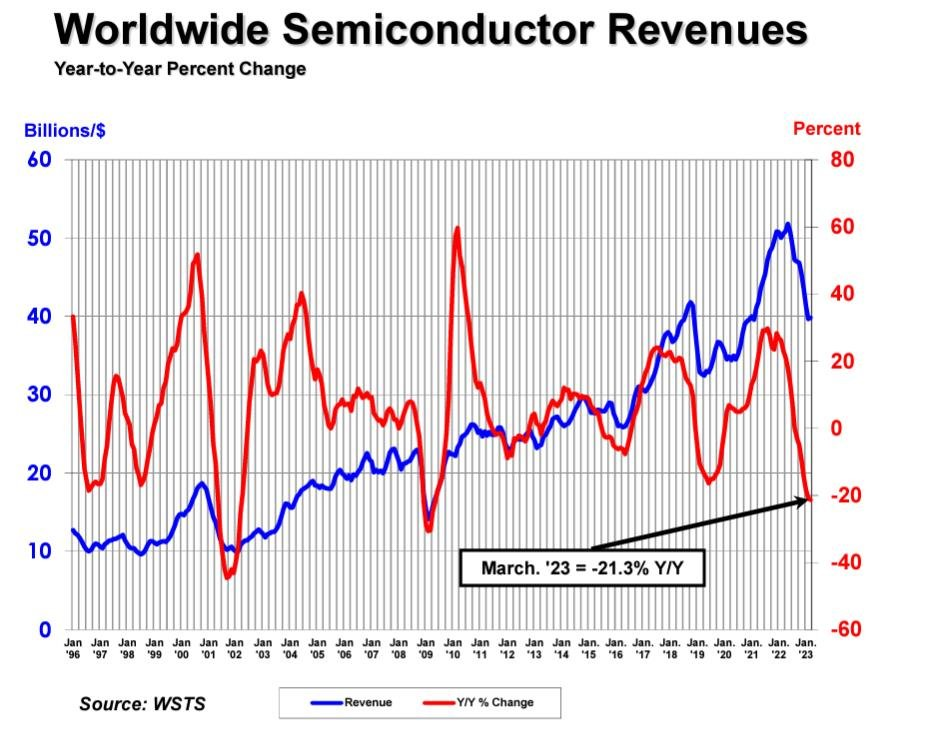

Recently, according to a report released by the Semiconductor Industry Association (SIA), global semiconductor sales totaled $119.5 billion in the first quarter of 2023, down 8.7% compared to the fourth quarter of 2022 and down 21.3% from the first quarter of 2022. Compared with February 2023, sales increased 0.3% in March.

From a regional perspective, semiconductor sales in Europe, Asia/Pacific/All Other Regions and China achieved year-over-year growth in March at 2.7%, 2.6% and 1.2%, respectively, but semiconductor sales in Japan and the Americas declined at -1.1% and -3.5%, respectively. Europe, Japan, the Americas, Asia/Pacific/All Other Countries and China (-34.1%) experienced year-over-year declines in semiconductor sales, with growth rates of -0.7%, -1.3%, -16.4%, -22.2% and -34.1%, respectively.

"Global semiconductor sales continued to decline in the first quarter of 2023 due to market cyclicality and macroeconomic headwinds, but monthly sales rose in March for the first time in nearly a year, providing optimism for a rebound in the months ahead," said John Neuffer, SIA president and CEO.

According to figures released by SIA, semiconductor sales in Japan increased slightly to 1.2 percent year-over-year in February, but Europe, the Americas, Asia Pacific/All Other Regions and China declined to varying degrees, with growth rates of -0.9 percent, -14.8 percent, -22.1 percent and -34.2 percent, respectively. Monthly sales declined in Europe, Japan, Asia Pacific/All Others, the Americas, and China, with growth rates of -0.3%, -0.3%, -3.6%, -5.3%, and -5.9 %, respectively.

In addition, according to 2022 semiconductor sales data by broad product category (called "end use"), the PC/computer and communication terminal markets account for about two-thirds of total semiconductor sales, while other markets are mainly automotive, industrial and consumer electronics.

However, according to the results of the Semiconductor End-Use Survey organized by the World Semiconductor Trade Statistics (WSTS), the sales of semiconductor end-use markets have changed significantly in 2022. Although the PC/computer and communication end-use markets still account for the largest share of semiconductor sales in 2022, the lead has narrowed. At the same time, automotive and industrial applications achieved the largest growth for the year. In addition, a McKinsey analysis shows that by 2030, automotive and industrial applications will account for 14 percent and 12 percent of the average growth in chip sales, respectively, thus driving demand growth in this decade.

How many chips does a car need?

How many chips does a car need?

Position and Function of Main Automotive Sensors

Position and Function of Main Automotive Sensors

Chip: The increasingly intelligent electronic brain

Chip: The increasingly intelligent electronic brain

LDA100 Optocoupler: Outstanding Performance, Wide Applications

LDA100 Optocoupler: Outstanding Performance, Wide Applications